- Open Banker

- Posts

- It's Time to Unbundle Banking

Jason Mikula is the Head of Industry Strategy, Banking & Fintech, at next-gen decision platform Taktile and the publisher of Fintech Business Weekly, a newsletter going beyond the headlines to analyze the technology, regulatory and business model trends driving the rapidly evolving financial services ecosystem. He also advises and consults for and invests in early stage startups. Previously, he spent over a decade building and scaling consumer finance businesses, including at Enova, LendUp and Goldman Sachs.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

The market for financial services is not static. It is inextricably intertwined with the rest of the economy – and society at large. Indeed, the market has historically responded to demand signals, rising to the occasion by innovating to provide new products and services and taking advantage of new distribution channels to meet consumers’ needs. Peer-to-peer payments apps like Venmo and Cash App, earned wage access services like DailyPay and Clair, and alternatives to traditional credit scores and underwriting are all recent examples of a market identifying and responding to consumer needs and preferences.

Notably, all of these innovations were initially developed outside of the so-called “banking regulatory perimeter” – even if banks later adopted them or launched comparable features.

Keeping Banks from Innovating and Innovators from Banking

The banking system itself often seems so averse to anything that could be deemed unorthodox that it’s difficult, if not impossible, to innovate within it. Yet chartered banks remain by far the dominant players in the US financial system, thanks in no small part to state and federal regulators: the gatekeepers that determine who is allowed to become or to buy a bank.

In the wake of the 2008 Global Financial Crisis, regulators themselves justifiably came under scrutiny, particularly the Office of Thrift Supervision, which had been responsible for supervising such banks as Washington Mutual and IndyMac, both of which failed during the crisis. Congress undertook significant regulatory reform. The most wide-reaching piece of that effort was Dodd-Frank, which:

Dismantled the Office of Thrift Supervision, with much of its authority and portfolio being transferred to the Office of the Comptroller of the Currency;

Created the Consumer Financial Protection Bureau and assigned to it the authority to enforce an expansive number of laws and regulations;

Added the Volcker Rule, which prohibited banks from engaging in short-term proprietary trading of derivatives, securities, futures and options;

Established the Financial Stability Oversight Council to monitor risks to the financial system from “too big to fail” firms;

Empowered the FDIC with orderly liquidation authority to manage banks’ failures in a more orderly manner;

Required derivatives to be traded on centralized exchanges, in order to provide greater transparency on firms’ off-balance-sheet exposure; and

Increased bank capital and liquidity requirements.

For the most part,[1] these reforms have been effective, recent history notwithstanding. But they have also had consequences, whether intended or not.

As a group of bank legal experts and advisors pointed out in an open letter to incoming regulatory leadership, from 2000 to 2007, an average of 144 bank charter applications were approved per year. But from 2010, the year then-President Obama signed Dodd-Frank into law, through 2023, a total of just 71 bank charters have been approved, or an average of five de novo banks formed per year.

The drought of new bank formation, combined with the inexorable pressure on existing banks to scale,[2] has led to much hand wringing about the ever-shrinking number of banks in the United States. Biden-era bank regulators' approach to this situation often appeared to be, at best, a desire to keep the problem from getting worse, or, at worst, misguided and counterproductive efforts to turn back the clock.

While I don’t personally harbor nostalgic feelings about some golden age of community banking, I’m also cognizant that a market dominated by a handful of mega-banks, as is the case in most other countries, is antithetical to the oft-stated public policy goals of fostering a dynamic and competitive free market.

Timmy’s Mom Lets Us Do Whatever We Want

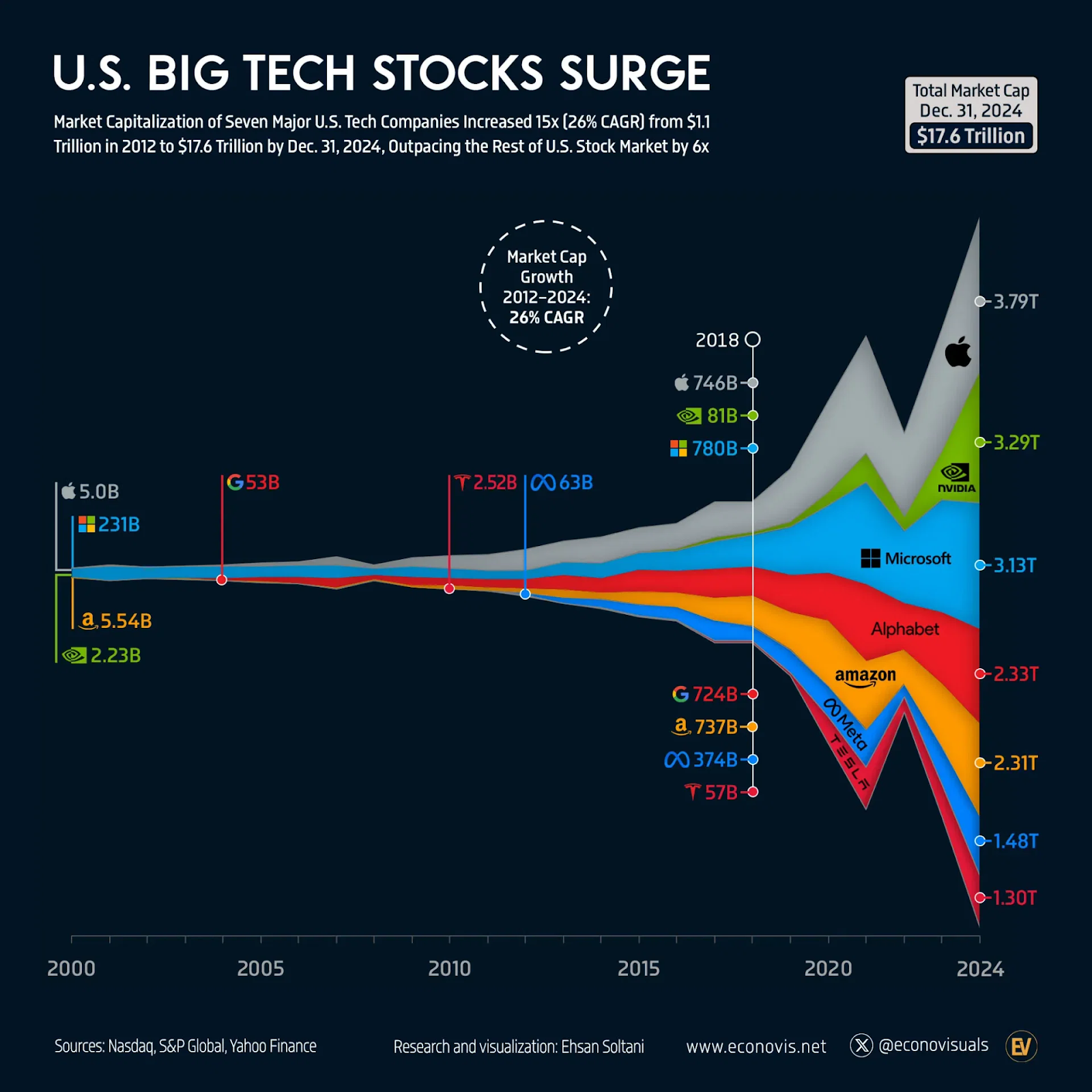

The decline in the number of chartered banks is hardly the only significant change in the financial system since the passage of Dodd-Frank. Technology firms and startups shifted from being a meaningful component of the economy and culture in 2010 to becoming dominant forces in a way few outside of Silicon Valley imagined possible. A sector that the public had once had largely positive views, even across partisan lines, finds itself not only at the center of today’s highly polarized political environment and culture wars but often a willing and active participant in them. This is perhaps no better exemplified than by the growth of the influence of Silicon Valley characters like Elon Musk, whom some are now referring to as “co-President,” and venture capital investors David Sacks, Peter Thiel and Marc Andreessen on government and public policy.

Image: Visual Capitalist

The growth of tech and venture capital has coincided with and powered the rise of fintech – thanks, in no small part, to Dodd-Frank’s Durbin amendment, which allows banks with less than $10 billion in assets – and their partners – to charge uncapped interchange fees. Consumer fintech offerings like Chime, Cash App and Current, which incumbent banks initially viewed with skepticism, have come to be significant players in the market for consumer financial services. Industry analyst Ron Shevlin’s survey research suggests that “digital banks and fintechs” account for 44% of new “checking” accounts: basically the same share as megabanks Chase, Bank of America, Citi and Wells Fargo combined (43%).

Much of the innovation and growth in lending is also taking place predominantly outside of the banking regulatory perimeter. Banks remain dominant in the market for consumer credit cards, with the top 10 issuing banks holding more than 80% market share.[3] But in other areas of consumer lending, banks have rapidly ceded ground to nonbank lenders. In 2013, for example, fintechs accounted for just 5% of the unsecured personal loan market, according to data from TransUnion. By 2018, that had jumped to a 38% market share, while banks’ share fell from 40% to 28% and credit unions’ share fell from 31% to 21%.

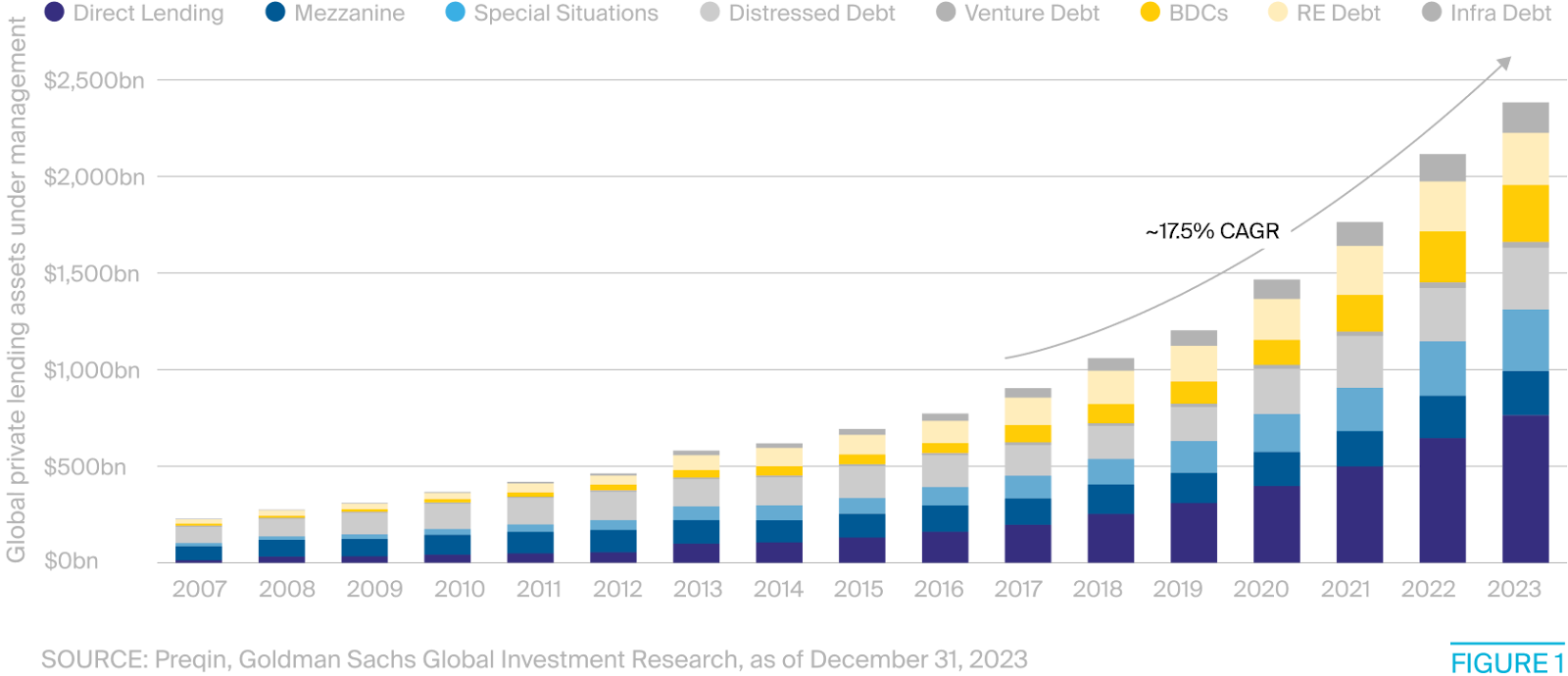

Moreover, innovation – particularly in serving the smallest loans and the lowest end of the credit spectrum – has nearly exclusively happened in the nonbank sector. While not without criticism (sometimes deserved), a plethora of earned wage access, overdraft avoidance, no-fee overdraft and cash advance products and services are attempting to meet consumers’ demand for credit that banks all too often serve with punitively expensive overdrafts, if not ignoring it altogether. Nonprime consumer lending is hardly the only credit product that has begun moving outside of the banking system. Residential mortgage lending, small business lending, commercial real estate, corporate and commercial finance and venture debt all increasingly take place outside of banks, helping to explain the explosion in private credit markets in recent years.

Image: BNY

The last 15 years have also seen the explosive growth of the crypto industry. Bitcoin, the original cryptocurrency, launched in January 2009. Today, the aggregate global market capitalization of crypto, including popular stablecoins like Tether and USDC, exceeds $3 trillion. While early crypto adopters tended to be anti-establishment, prizing the idea of a currency or asset that existed outside of government-regulated financial systems, the orientation of many crypto advocates today is the opposite: They now seek the perceived legitimacy – and access to traditional financial markets – that comes with legislative and regulatory recognition. Though greater integration of crypto into traditional financial markets and the banking system seems inevitable at this point, like much of fintech to date, crypto developed and largely exists outside of the banking regulatory perimeter.

Time to Build (An Unbundled Regulatory Structure)

Per a famous saying in business, there are only two ways to make money: bundling and unbundling.

The “business of banking” in the US has long consisted of the bundle of holding insured deposits, making loans and facilitating payments. However, whether or not the banking industry and its regulators acknowledge it, we are and have been in an era of unbundling, or, put differently, an area of disaggregation and specialization. This evolution has the potential to improve efficiency and with it access, inclusion and, yes, profitability.

What might this look like in practice? Perhaps not so different from the place where market forces have already led us. Bank-fintech partnerships, like those that enable consumer neobanks like Chime and non-bank lenders like Affirm, already represent a kind of division of labor.

But recent history suggests allowing much of fintech and crypto to develop outside of the banking regulatory perimeter has been a mixed bag. Regulation, supervision and enforcement have also failed to keep pace with how the market has evolved. Despite crypto and fintech largely existing outside of the banking regulatory perimeter, the risks they pose can and have been transmitted into the banking system – occasionally with catastrophic, if not systemic, consequences.

Rather than deputizing banks to police these risks, or ignoring them altogether, wouldn’t it be preferable to make fintech and crypto firms more accountable by bringing them under direct regulatory supervision? Here are some possibilities:

E-Money license: The concept of an electronic money, or e-money, license has already taken hold in many other countries. Such licenses typically allow a firm to issue and manage electronic money, provide payments services, offer digital wallets and prepaid cards and manage payment accounts. Critically, e-money institutions are generally not permitted to hold deposits, but rather must hold customer funds for safekeeping, most commonly at an insured depository. In practice, this operating model resembles how firms like Chime work with their bank partners today, with the distinction that under an e-money regime, a firm like Chime would be licensed and directly supervised.

Payments institution license: Payment institution licenses, common in other countries, typically include a narrower set of permissible activities than EMIs, such as execution of payment transactions, issuing of payment instruments, payment initiation and account information services, but not the issuing of e-money. Such a license could allow an entity to access payment systems like ACH, FedNow or a Fed master account without the need to work with a bank partner. Such licenses could be issued by a competent federal authority, such as the OCC, with corresponding direct regulatory supervision.

Nonbank lending license: The major driver of fintechs partnering with banks in lending businesses stems from the lack of a federal nonbank lending license. Without a bank charter or bank partnership, lending firms must obtain licenses in each state they wish to operate, which have widely varying requirements and criteria around loan sizes and permissible interest rates. This might have made sense when most lending took place in person. But in 2025, with most routine financial transactions taking place online, the existing state-by-state model is no longer fit for purpose. A federal nonbank lending license, with accompanying direct regulatory supervision, solves this problem while enhancing consumer protection vs. the existing bank-fintech partnership model.

Crypto and/or stablecoin licensing: While I personally remain a skeptic of the utility of crypto, there’s no denying the industry has demonstrated staying power, having survived through 2022’s “Crypto Winter” and multiple cycles of ups and downs. The current patchwork of SEC, CFTC and state regulation is, at best, incoherent; assuming the mission is to protect consumers and investors, it is also an abject failure. If crypto is here to stay, an approach to licensing and supervision that follows the “same activity, same risk, same regulation” principle would be a meaningful improvement compared to the status quo, which allows for pump-and-dump “meme coins.”

For better or for worse, President Trump has dramatically thrown open the Overton window of what is possible. While some in industry may gravitate toward a more laissez-faire approach – eschewing true chartering, licensing and regulatory reform in favor of a more hands-off approach from government, coupled with self-regulatory and “standard setting” efforts – that is a mistake. Instead, policymakers, regulators and industry should use this opportunity to enact meaningful updates to better align the regulatory establishment with where the financial service industry is today, and where it’s going in the future, rather than continuing to look to the past..

The opinions shared in this article are the author’s own and do not reflect the views of any organization they are affiliated with.

[1] FDIC Office of the Inspector General, “FDIC Readiness to Resolve Large Regional Banks,” FDIC, December 2024.

[2] Another effect of the regulatory burdens of Dodd-Frank. Compliance costs don’t scale linearly with size, so larger banks have a comparative advantage over their smaller rivals in meeting those costs.

[3] Not terribly surprising – recall that Visa didn’t IPO from its bank owners until 2007.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

If an idea matters, you’ll find it here. If you find an idea here, it matters.

Interested in contributing to Open Banker? Send us an email at [email protected].