- Open Banker

- Posts

- We Don't Need CAMELS and Stress Tests for Banks That Don't Need Bailouts

We Don't Need CAMELS and Stress Tests for Banks That Don't Need Bailouts

Written by Alexei Alexandrov

Open Banker

June 24, 2025

Alexei Alexandrov consults various non-profits, including working on housing and mortgage regulation proposals at the Urban Institute and advising on mental healthcare and homelessness research and interventions in Allegheny County (PA). Prior to that, Alexei served as the chief economist of the Federal Housing Finance Agency, worked in management and director roles at Amazon and Wayfair, and served as a senior economist and a fellow at the Consumer Financial Protection Bureau. Alexei received his Ph.D. from Northwestern University, taught at the University of Rochester, and published academic articles on topics including antitrust and consumer finance.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

“There is little reason to heavily regulate banks that can absorb their own financial risks”

That’s a quote from the Heritage Foundation’s glowing review of the CHOICE Act (“the Act”) – a bill proposed by Congressman Hensarling (R-Texas), and that passed the House in 2017, but could not get 60 votes in the Senate. The Act would have given banks a choice between the current prudential regulatory system and having more capital.

Yet banks still receive bailouts. The alleged resiliency of the banking system during the pandemic is in many ways illusory: these institutions were heavily supported by the Fed more than doubling its balance sheet, generous federal policies keeping borrowers even better than before (including mortgage forbearance and a trillion dollars in stimulus checks just in 2020-2021), and a new line of business with the Paycheck Protection Program (PPP) and its about 800 billion in (mostly forgiven) small businesses loans.

At the same time, banks remain highly regulated and heavily supervised. So much so that there is pressure for broad regulatory relief from the Trump’s Administration, and hundreds of federal bank examiners are losing jobs.

It’s time to reconsider an improved version of the safety and soundness regulatory relief parts of the Act.

I propose offering banks a choice to use more capital and, as a result, get relief from virtually all other safety and soundness requirements, lower FDIC insurance, and mergers subject only to the Department of Justice’s antitrust approval. The Administration and Congress could have the best of both worlds by getting a safer banking system (and not getting blamed for the next round of bailouts that will inevitably come otherwise) and less regulation. This would also increase demand for Treasuries, lowering their yield, and in turn lowering the deficit and interest rates for everyone. Near the end of this blog, I briefly argue that, as currently framed, both alternatives under discussion by the Administration would marginally increase the likelihood of future bailouts and could make it even harder for community banks to compete against the largest banks in the country.

Skin in the Game or Examiners in Your Building

If a bank chooses to have sufficiently more capital than current thresholds, then the bank gets relief from many safety and soundness (prudential) regulations. The economic rationale is simple: more skin in the game (capital) lessens the need for safety and soundness regulations.

The price for banks to be eligible:

Sufficient capital (details below), with short-term Treasuries holdings the sole exception from capital requirements; and

At most a minimal exposure to derivative trading.

The benefits for eligible banks:

Safety and soundness/prudential regulations and exams limited to ensuring that the requirements above are actually satisfied (checking exclusively for fraud or gross incompetence, obviating the need for CAMELS ratings for qualified banks);

FDIC guarantee fee at the minimal level – 1 basis point or less; and

Fast-track merger review by the Department of Justice as long as the resulting combined bank is still eligible as above.

Below that, there are some implementation nuances.

Simpler capital ratios. The more sophisticated ratios assign risk-based weights to different types of assets, with higher credit risk assets requiring more capital. This program would, instead, employ a simpler unweighted ratio – like the community bank leverage ratio (introduced by EGRRCPA in 2018) are easier to compute and monitor, and could be more stable against unexpected risks.

Mark-to-market where practical. Two still-unfixed issues heavily contributed to the 2023 bank failures, and leave many banks still susceptible to the same issues: (i) ratios that assigned no risk weight to government MBS and long-term Treasuries and (ii) allowing banks to report assets at historical value as opposed to the actual (“mark-to-market”) value. This policy should apply mark-to-market for easier-to-value assets like longer-term Treasuries or MBS holdings. Reasonable regulators can draw the line of “easier-to-value,” but Treasuries and government MBS are in.

No capital required for short-term Treasuries. Short-term Treasuries (3-months or less) are effectively risk-free, and should be an outlet for banks that can’t or don’t want to attract more capital but still want to take in more deposits, or that want to increase their capital ratio without getting more capital. With the abysmal interest rates banks pay on deposits, banks still make money by investing in short-term Treasuries. Increased demand for short-term Treasuries allows the US Treasury to shift its debt structure towards more short-term debt and less long-term debt. By restricting the long-term Treasury supply, the long-term Treasury yields will decrease even if long-term Treasuries require capital.

A special case of this exception is government MMFs, stablecoins, and narrow banks, where their assets are solely short-term Treasuries. These entities would not require capital at all, but could become banks without worrying about over-regulation (simply audit-like exams), and still advertise FDIC insurance (while paying almost nothing for it, for a good reason as they’d be ultra safe).

Vanilla-only and minimal exposure to derivatives. Barely any banks trade derivatives at scale, but derivatives are key to many counterexamples for why sufficient capital requirements are not enough. The top 6 banks by derivative dollar value account for over 95% of the overall bank derivative dollar value. The vast majority of these positions are interest rate risk contracts, most of that is for terms under 1 year, and half of interest rate contracts are centrally-cleared. Thus, limiting derivatives to (i) interest rate contracts only, (ii) with under 1 year duration, (iii) central clearing, and (iv) limited exposure (under, say, 10% capital) would effectively allow for business as usual at all banks except for about a dozen.

Audit-like exams. Regulators should ensure that there is no fraud or gross incompetence, and could make non-binding recommendations and collect data for analysis. These exams would be factual and fast, and mostly result in no follow-ups. There would be no need even for CAMELS rating, as all letters except for “M” would be subsumed by the qualification requirements.

Mergers subject only to DOJ approval. High capital and other requirements above would keep the system safe, obviating the need for prudential merger review. However, we should still address antitrust concerns. Even a merger between the top two non-G-SIBs (US Bank and PNC) would create a bank about 1.5 times smaller than either Citi or Wells (the smaller two of the top four). The DOJ has the expertise to decide quickly whether, say, the only two banks merging in a remote county without online banking penetration, without slowing down for prudential concerns.

FDIC insurance. The current FDIC insurance is not sufficiently tailored to risk. Sufficient capital combined with minimal derivative exposure (or investing in short-term Treasuries) is less likely to fail by an order of magnitude – effectively, there is a very large deductible (or nothing to insure). Accordingly, charging a token amount (say, 1bp) would increase the incentives to use capital and for nonbanks to come out of the shadows into banking.

Off-ramps. A qualified bank might find itself with a slightly lower ratio than the threshold, especially with mark-to-market assets. Regulators should have a reasonable grace period for banks to catch up, but perhaps trigger a higher FDIC insurance rate for that period and a sufficient shortfall. The exceptions should be larger banks combined with fast deterioration, where regulators might need to step in as soon as possible.

Off-balance sheet items. Similar vanilla standards should apply to off-balance sheet items. Banks can still extend lines of credit, but either these lines of credit are actually guaranteed through downturns (and thus should be the subject to capital requirements) or these lines of credit are not guaranteed through downturns (and should be advertised accordingly – you’ll get the line of credit but only if you don’t need it – for both businesses and credit cards).

Limited exposure to non-bank financial institutions (in the future?). Banks lending to private equity and hedge funds have reasonable critics. Banks’ exposure to private credit is growing, but is still relatively low. Regulators could set a simple limit on the share of a bank’s assets that are used for private credit lending. In contrast, loans to, say, non-bank mortgage companies to increase liquidity to originate and service government-backed mortgages could simply be subject to standard capital requirements.

Who Holds the Cards… and Who is Bluffing?

Community banks already have capital, but I’m pretty sure the behemoth banks -- ironically the ones calling for regulatory relief with the loudest megaphones – would not opt-in. Calling their bluff allows regulators to focus resources exactly where they are needed the most.

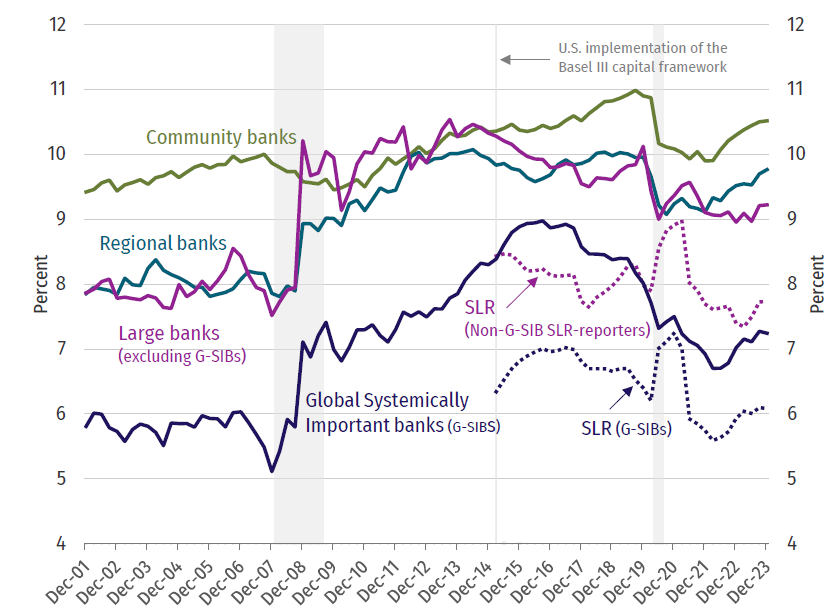

The following Figure shows how banks of different sizes use capital:

Community banks have more capital (despite larger banks having higher regulatory thresholds)

Pre Financial Crisis:

At the largest banks, capital ratios were indeed abysmal by 2007,

At the community banks, capital ratios were much better.

The largest banks are in better shape now than they were pre-crisis, but by how much?

Yes, 7% in 2023 is about 20% more capital than 6% in 2006, but are we sleeping that much better knowing that G-SIBs are only leveraged 14:1 now as opposed to 17:1 at the end of 2006?

Figure: evolution of capital ratios, by bank type

Hensarling proposed a 10% supplementary leverage ratio (SLR) threshold. Given the pandemic and 2023 experiences, we likely need more than we thought we did in 2018. As a ballpark number, let’s say 12.5% SLR – an 8:1 leverage, that should be within reach of community banks, with many likely already there.

For the largest banks, moving to 12.5% is unlikely. That doubles their current capital levels and, while fantastic for financial stability, it is hard to see G-SIBs making such a choice.

This Isn’t Capital Punishment

A frequent objection to higher capital requirements is that it will limit how much lending a bank can do, slowing down the economy. But capital is not cash in the vault. Instead, capital is the bank's shareholders’ equity, relative to the leveraged debt.

When a person gets a 20% downpayment mortgage (20% capital ratio), the downpayment still goes towards the purchase. Lenders require a downpayment so that the borrower absorbs the first hit if the house price decreases, and still has an equity cushion to maintain the house.

Bank capital requirements are similar (see also: insurance deductibles, as the FDIC is insurance for banks). Banks shouldn’t go underwater whenever there is a minor shift in asset prices, spurring bank failures, and in turn less lending and an economic slowdown.

For example, 6% capital means that a 7% decline in asset values wipes out the bank shareholders, and the bank is underwater (7% decline is comparable to a bank holding 10-year Treasuries with 1% interest rates, and then rates increasing to 2%). If the bank still operates, bank management could either be ultra conservative (circa 2008) or could realize that a gamble could get enormous returns and there is nothing to lose (as did many S&Ls in the 1980s, exacerbating that crisis).

In contrast, a 12.5% capital requirement enables a bank to sustain much larger losses and still be sufficiently above water (potentially able to sustain a hit of a 3 percentage point increase of MBS interest rates, depending on bond convexity and duration – comparable to the difference between January 2020 and 2025).

The other objection to capital requirements is that capital is more expensive than debt, and that could result in higher loan interest rates. But a fundamental finance theory theorem (both authors, Modigliani and Miller, received Nobel prizes) shows that a firm’s capital structure is irrelevant for the firm’s value. The discounted future cashflows and the associated risks matter, while the capital structure simply rearranges who exactly claims these cashflows and when. Suppose equity is more expensive than debt in the current structure. Then, increasing equity is costly, but it also lowers the cost of debt even further because debtholders are even better protected by a larger equity cushion, canceling out any cost of the equity increase.

The main real-world difference from the theoretical theorem is that interest on debt is tax deductible, so we give banks (and other firms) a tax break for having less skin in the game. There is no sound basis for this, as proved by capital/debt ratios outside of banking. The infamous “greed is good” leveraged buyouts of the 1980s were financed with more than 10% equity – roughly double the skin in the game that G-SIBs have right now. Today, private equity buyouts are closer to 50% equity – an unthinkable amount of skin in the game for banks. The second adjustment is more bank-specific: if bondholders believe that a bank is Too Big To Fail, then bondholders don’t care much about an equity cushion.

A higher interest rate on loans due to increased capital is efficient – it either increases tax revenue and decreases deficit by taking away a tax break that gives wrong incentives, or it decreases the TBTF discount. And, even assuming a historically-large equity increase and full pass-through to consumers, it’s still an under 10 basis point interest rate increase.1

Free to Choose versus marginally moving the goalposts every four years

Today we are stuck in the worst of both worlds, with banks stuck with poorly targeted and burdensome supervision and citizens stuck with bearing the socialized losses when undercapitalized banks fail. We also have a unique opportunity to fix both, recapitalizing banks and refocusing risk management to only those that are unable, or unwilling, to properly capitalize themselves. Let’s make the choice to give banks the choice.

Instead, at least based on high-level publicly-available descriptions, the Administration is discussing two alternatives. The first alternative is marginally lowering one of the capital ratios (SLR) – the new maximum leverage allowed could be closer to 25:1 or 30:1 instead of the current 20:1. Such a change would bring the largest banks even closer to 2006 levels of barely any skin in the game, is irrelevant for community banks as they use more capital than required (and would give the largest banks even more advantages than they currently enjoy), and would provide no relief in dealing with examiners or following burdensome regulations. It is also likely to do little for stoking demand for Treasuries, as the capital relief is to the broad ratio, as is already getting noted. As importantly, this change would likely get rolled back quickly under a different administration, so it would be hard for banks to build a long-term strategy around it.

The second alternative is exempting Treasuries and Fed account holdings from the same capital ratio calculation. The same broad concerns apply here because long-term Treasuries have interest rate risk, as SVB just reminded us two years ago. A much safer version of this alternative is to leave longer-term Treasuries (say, over 90 days) under the current capital requirement umbrella. Between Treasury deciding how much short-term versus long-term debt to issue and the Fed managing its enormous balance sheet, these two entities could easily translate increased demand for short-term Treasuries and Fed account holdings into increased demand for long-term Treasuries, all without increasing bailout risk, and with a more direct impact to Treasury demand than lowering the broad capital ratio. This still does nothing for community banks or actual regulatory relief, and still simply slightly moves the goalposts until another Administration though.

The opinions shared in this article are the author’s own and do not reflect the views of any organization they are affiliated with.

[1] Suppose a bank wants to increase its equity ratio from 9.5% to 12.5% – a very high increase historically, see Figure above. Banks’ return on equity is around 10.4% over the last decade. Banks’ marginal funding likely comes from something close to the Fed Funds Rate of around 4.3%, or somewhat higher. At least some Modigliani and Miller logic applies of more equity making debt cheaper (with half being a typical educated guess). Thus, the rate increase due to the cost of capital would be roughly (12.5%-9.5%)x(10.4%-4.3%)x1/2=9bps. As brief as it is, this footnote arguably contains a more detailed economic analysis than the 300+ Federal Register pages of the much-discussed Basel Endgame proposal.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

If an idea matters, you’ll find it here. If you find an idea here, it matters.

Interested in contributing to Open Banker? Send us an email at [email protected].