- Open Banker

- Posts

- Let a Thousand Fintech Banks Bloom

Todd H. Baker is a Senior Fellow at the Richman Center for Business, Law & Public Policy at Columbia Business School and Columbia Law School and the Managing Principal of Broadmoor Consulting LLC.

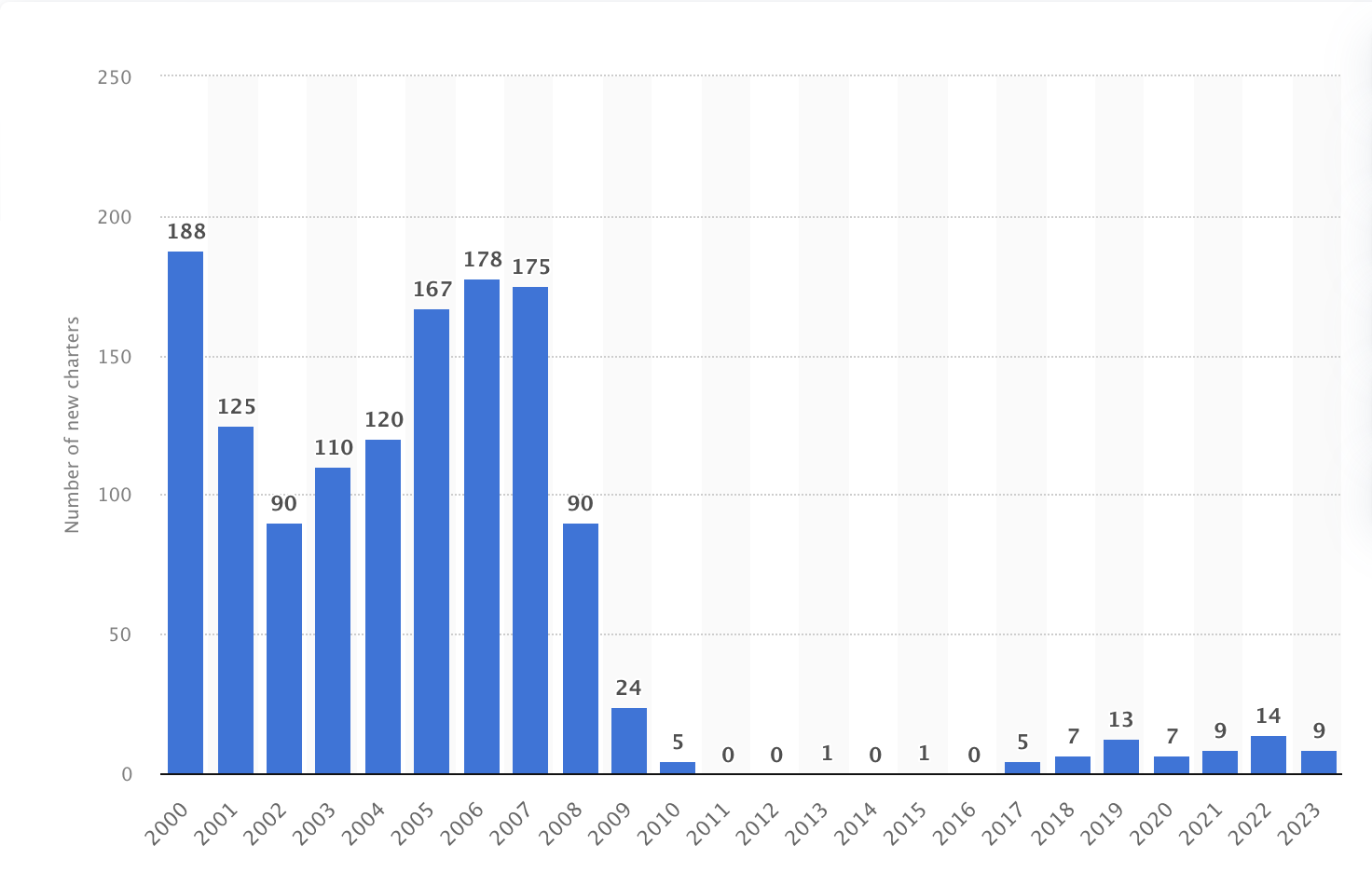

The decline in new bank formations is a sad but familiar story. Roll the tape back and recall that 144 new bank charters were approved on average every year between 2000 and 2007. In contrast, only 71 total new banks were approved between 2010 and 2023, including four years in which no new banks were approved at all.

It's far past time to change that dynamic. We need many more new banks to increase competition and spur innovation. More than that, we need to ensure effective oversight of our quickly evolving financial system, where customers are voting with their feet to get more and more of their services from non-banks. Today, 88% of U.S. consumers use fintech apps to manage their finances. The B2C fintechs are ready to fill the gap of bank formation, if only we will let them become banks.

Stalling the Engine of Financial Innovation

What caused the crash in new bank numbers over the last 15 years? Low interest rates were certainly a major factor as they challenged the profitability of traditional community banking.

At the same time, the banking market itself was changing, as both new nonbank fintechs and technologically sophisticated large banks used the digital revolution to provide products and convenience that small banks struggled to match. This blunted some of the local delivery and personal service advantages of community banks and made competition for personal banking, in particular, very challenging when conducted along traditional lines.

But there was more happening behind the scenes. While traditional community bank charter applications were down, interest in new bank charters remained very active among fintechs. Many of the new inquiries fielded by regulators over the last decade were from B2C fintechs – digital nonbanks engaged in “neo banking,” national lending or payments. (I’m talking here about B2C fintech, not crypto banking, which is another topic entirely and raises an entirely different set of concerns.) In short, the entrepreneurs who historically would have founded a bank saw more opportunity in fintech – you can find the missing charter applications in a decade of Series A press releases.

Convertible Debentures

Today, these fintech founders see in a bank charter an attractive vehicle for business model and funding stability, revenue enhancement, customer retention, and cross-sell. Nonbank fintechs have learned that providing bank-like services without a charter is a costly and complicated exercise, since banks alone have direct access to deposit funding, the payments and card rails, and national lending. And when they share that access, they charge dearly for it.

While the “partner banking” model allowed fintechs indirectly to provide banking products and services to their customers, it also entailed a loss of control over critical aspects of customer experience. Contractual and technical constraints associated with the small size and inadequate technology stacks of partner banks made it increasingly difficult to compete on even terms with the dominant mega banks in the B2C space. Compliance, too, became a serious problem, as bank regulators, partner banks and fintechs struggled to draw lines of responsibility between customer-facing fintech providers and back-end partner banks.

As the weaknesses of the partner banking model were exposed, the benefits of a banking charter came into focus for fintechs. For lending-focused fintechs, deposit insurance would enhance stability, profitability and customer retention, while national lending preemption would simplify operations and reduce costs. For payments-focused fintechs, deposit insurance would significantly increase the ability to hold and manage customer funds and provide many new avenues for growth and profit.

These benefits were long thought to be largely offset by the capital, operations, and compliance costs associated with banking regulation. But developments with the partner banking model means that most of the requirements of a bank license, such as BSA/AML, consumer compliance, CRA, cyber and other risk management, capital and liquidity management – and their associated costs – have either directly or indirectly become the responsibility of front-end fintechs.

Despite the potential advantages of bank charters, fintechs have had a nearly impossible job joining the commercial banking club in the last decade. During the first Trump administration, for example, only one fintech national bank was approved, while two fintech lenders received bank M&A approvals and one fintech industrial bank was approved by regulators. Other fintechs were actively discouraged from trying, a message that the Biden administration intensified. It has been nearly five years since the FDIC last approved insurance for a de novo fintech bank and three years since the last fintech bank acquisition was approved by the OCC and the Fed.

The effort by acting Comptroller Brian Brooks to issue national banking charters for non-deposit-taking fintechs and payments providers during the first Trump term got bogged down in litigation which couldn’t even begin to be resolved until one of the novel charters was approved – a catch-22 that prevented anyone from trying. Fintechs have been forced to continue paying for increasingly expensive and restrictive partner banking services or driven to pursue fringe solutions, such as uninsured trust charters, uninsured state banks and the like.

Standing Athwart History

So, if the case for reviving new bank formation partly by leaning into the fintech revolution is so clear, why hasn’t it happened? What has caused the regulators to effectively shut down the pipeline of new bank and M&A applications from fintechs?

We know that performance of small banks in general is not the issue. As Fed Governor Bowman noted recently, small banks frequently outperform larger banks during periods of stress, as we saw during the Covid pandemic, the 2008 financial crisis and the 2023 midsized bank episode. Fintech banks would pose different risks than traditional community banks, of course, but those risks should be manageable with proper oversight.

The ”something else” that was going on in regulatory agencies was a dramatic tilt toward conservatism in bank chartering decisions. This had two causes. One was the 2008 financial crisis—a crisis that new banks neither caused nor contributed to in any meaningful way. While the largest banks have rightfully faced tougher oversight for their outsized and interconnected risks, some of that conservative attitude has trickled down to low-risk new bank chartering decisions—decisions that don’t move the needle on financial stability or the overall health of the financial system, unless, of course, you stop issuing any charters at all.

The second reason for conservatism was the speed at which fintech was changing B2C finance. Bank regulators are always concerned that they don’t fully understand idiosyncratic and correlated risks associated with new developments in banking. They have often found themselves behind the curve when markets evolve quickly, as they did prior to 2008. But the analogy fails in the case of B2C fintech. Because fintech works through partner banks today, there is enough experience and history for the risks to be fully understood, as long as regulators pay attention (I’m casting a gimlet eye at the Federal Reserve Board, Synapse, and Evolve Bank). But the conservatism remains.

This has led to a familiar type of regulatory foot dragging which distorts the de novo process. When regulators are insecure about risk, they frequently “play the clock” by greatly extending processing times, “suggesting” application withdrawals and/or refilings, adding enormously expensive pre-opening hiring requirements and the like, which make the approval process a nightmare for all but the most persistent and well-funded applicants (this is an area of process that needs serious reform).

It’s not that the regulators couldn’t charter more fintech banks if they chose to. They have all the power they need under existing law and practice to charter insured fintech-focused banks that take deposits, have full payment system access and are subject to comprehensive regulation tailored to their specific business plans and risks. With appropriate guidance and oversight, these fintech banks could deliver innovative services to consumers and businesses while maintaining safety and soundness.

The days of “move fast and break things” or “ask forgiveness not permission” are over in B2C fintech. Today’s fintechs are far more mature than those a few years back. They have already learned the hard lessons about risk management, compliance and money laundering in their interactions with customers and partner banks. There’s really not much in an insured bank charter for a fintech – or a regulator – to be afraid of.

Give Yes for an Answer

I’d argue that regulators should be rushing to issue fintech bank charters. It’s a truism of banking regulation that society is better off if banking activity is kept within the regulatory perimeter rather than split between regulated banks and unregulated nonbanks. The latter situation frequently results in a race to the bottom, as we saw in the mortgage business prior to 2008. Bringing neo banking and B2C fintech inside the bank regulatory tent will allow better systemic supervision and more effective risk management by bank regulators, which will be good for all of us. As Michele Alt of Klaros Group is fond of saying: instead of tut-tutting about risks in the “shadow banking system,” regulators should demand that fintechs get bank charters in order to protect the millions of consumers who now get their financial services through fintechs.

So, let a thousand fintech banks bloom!

The opinions shared in this article are the author’s own and do not reflect the views of any organization they are affiliated with.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

If an idea matters, you’ll find it here. If you find an idea here, it matters.

Interested in contributing to Open Banker? Send us an email at [email protected].