- Open Banker

- Posts

- DOGE the Fed: Narrowing the Federal Reserve System’s Focus to Monetary Policy

DOGE the Fed: Narrowing the Federal Reserve System’s Focus to Monetary Policy

Written by Alexei Alexandrov

Open Banker

January 28, 2025

Alexei Alexandrov consults various non-profits, including working on housing and mortgage regulation proposals at the Urban Institute and advising on mental healthcare and homelessness research and interventions in Allegheny County (PA). Prior to that, Alexei served as the chief economist of the Federal Housing Finance Agency, worked in management and director roles at Amazon and Wayfair, and served as a senior economist and a fellow at the Consumer Financial Protection Bureau. Alexei received his Ph.D. from Northwestern University, taught at the University of Rochester, and published academic articles on topics including antitrust and consumer finance.

There has been some talk about whether there could be more government efficiency in the way we regulate and supervise banks.

Of course there can!

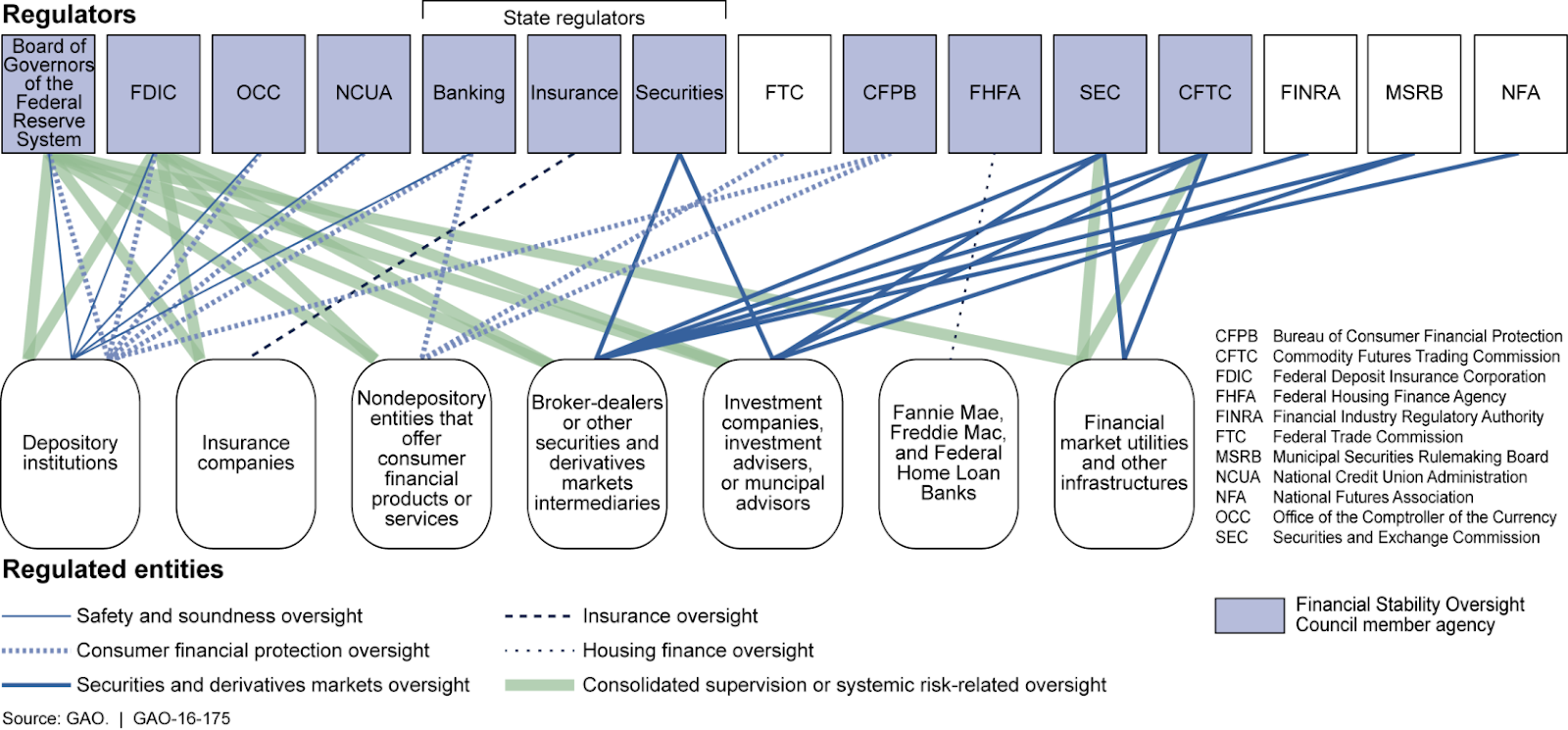

The Government Accountability Office (GAO) titled its 2016 report “Complex and Fragmented Structure [of financial regulation] Could Be Streamlined to Improve Effectiveness.”[1] And the GAO – charged with eliminating waste, fraud, and abuse in the Federal government, the agency that had this mission before the Department of Government Efficiency (DOGE), and will continue after DOGE wraps up – does not say things like that lightly. Just look at the spaghetti chart of financial regulation GAO created for its report!

The Federal Reserve System (the Fed) stands out with the greatest number of duplicative responsibility lines on the spaghetti chart, is unpopular across the aisle, and also has by far the most employees (and arguably the best paid). In short, how would we DOGE the Fed?[2]

I would start by separating the things the Fed does that deserve the special independence from the Congress and the President that the Fed enjoys from the things the Fed does that other, non-independent, agencies do, and could efficiently absorb.

What Does the Fed Do?

The Fed, in its own words, has the following five “functions:”

1. “monetary policy;” (mainly through setting interest rates)

2. “minimize and contain systemic risks;”

3. “safety and soundness of individual financial institutions;”

4. “payment and settlement system safety;” and

5. “consumer protection.”

Monetary Policy should remain with the Fed, as they have a unique mandate in maintaining price stability and maximum employment (not even on the GAO’s chart), and that mandate is one we have strong policy reasons for insulating from the political process. I am effectively proposing shrinking the Fed’s set of responsibilities much closer to that of conducting monetary policy and the classical lender of last resort.

The other responsibilities should shift to the Department of Treasury (including the Office of the Comptroller of the Currency), the FDIC, and the states. This rearrangement would introduce better accountability throughout financial regulators by assigning clear roles and responsibilities, and would let each part of the government become focused on its one key mission. It would also allow the Congress and the President to control the financial regulation agenda, as both parties have been frustrated by the Fed’s use of its independence to resist changes in prudential regulation and systemic risk management.

Why Monetary Policy Requires Independence

The Fed’s independence is typically framed in terms of monetary policy, and in particular the ability to set interest rates to combat inflation. Shielding the Federal Reserve (“the Fed”)’s ability to set interest rates from short-term political pressure is crucial to maintaining price stability.

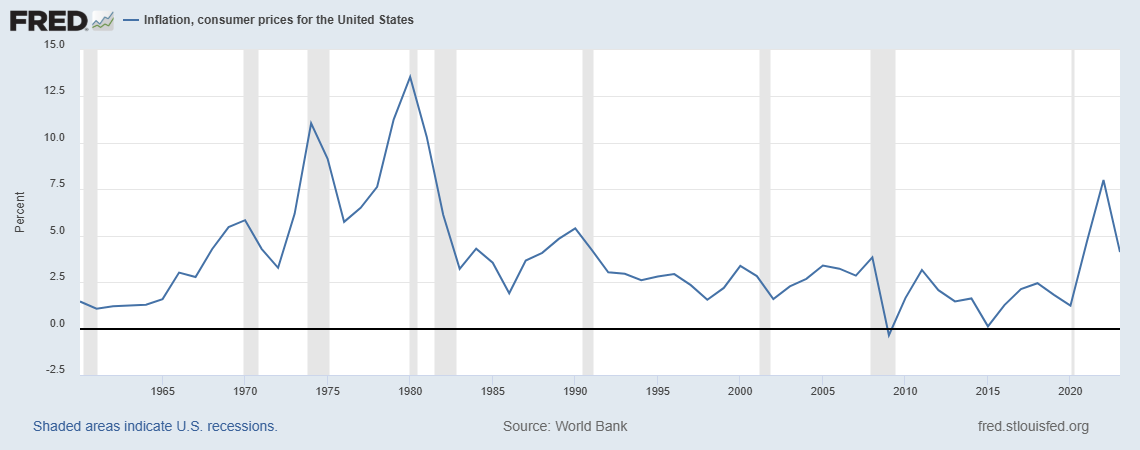

The relatively-weak Fed chair during the 1970s shares the blame for the only prolonged episode of high inflation in the US in the last sixty years.[3] Other than the 1970s, the Fed has a pretty good inflation record.[4]

Meanwhile, there are still demands from the leaders of both parties that the Fed lower interest rates. Lower interest rates have immediate political benefits (higher employment, higher profits, ZIRP filling everyone’s pockets with cash). The consequences (inflation, financial crisis) come later. Any rational President or Congress has an incentive to lower interest rates in order to get reelected, but we have an incentive to avoid runaway inflation in the long run. So we tied ourselves to that mast and gave the Fed the power to take away the punch bowl no matter how much we want another drink so that we don’t have a hangover in the morning. Let’s keep that rope in place.

What About the Rest?

The rest of the Fed’s functions are already performed – duplicatively – by Executive agencies that are more accountable to the President and have other critical checks and balances, from oversight to cost-benefit analysis. There are politicization risks here, of course. For example, relaxing supervision requirements to help bankers make more money and to garner political contributions. But these changes take years to percolate through the system, with no immediate political popularity uptick and risk political blowback, particularly if they result in a downturn or crisis. So what can we safely move back to Executive agencies?

Minimizing Systemic Risks (Financial Stability)

In the run-up to the Financial Crisis, the Fed dramatically missed the importance of each of the following: the fragility of overleveraged financial institutions (30:1); collateralized debt obligations (CDOs) and credit default swaps (CDSs) interconnecting the financial system prone to repo runs; and the danger that the rapidly deteriorating mortgage lending standards could spark a fire throughout the financial system.[5] The heroic and ingenious rescues prevented the resulting recession from being much worse. But that shouldn’t diminish the point that the Fed only started acting when it was too late.

The Congress noticed, and the Dodd-Frank Act created the Financial Stability Oversight Council (FSOC) within the Department of Treasury.[6] FSOC is supposed to fill the gap of financial stability oversight and monitoring across financial institutions, as the Fed did not do that job well. The Fed Reserve chair is on FSOC, so the Fed’s input is preserved, but we have a single-responsibility agency fully accountable to the President.[7] It’d be a miracle if the Congress got FSOC’s design and powers exactly right the first time, so no doubt it will be work in progress, with each party pushing in a predictable way, but this progress will be driven in exactly the same administrative way as with other executive agencies, without the unnecessary shield of extra political independence.

Safety and Soundness (Supervision)

The Fed oversaw the failure of Silicon Valley Bank (SVB) in 2023. SVB experienced an incredibly-fast bank run, with many blaming Twitter. But the underlying cause was too much exposure by SVB in long-term Treasuries and MBS, with the Fed’s rate increase lowering the value of SVB’s assets, resulting in SVB being effectively underwater. This is the same issue as we had in the Savings and Loan crisis in the 1980s, so it’s something that the examiners and the Fed’s management should have been intricately familiar with. Moreover, the Fed itself raised the rates – so if anyone knew that this was going to be an issue ahead of time, it was the Fed.

The Federal Deposit Insurance Corporation (FDIC) didn’t do better with a similar Signature Bank fail, but the FDIC (and the Office of the Comptroller of the Currency, OCC) didn’t do worse, despite not being the ones deciding on interest rates and not having the degree of independence that the Fed has. If anything, in light of these bank failures, the GAO has issued a report in late November 2024 (so, naturally, nobody noticed) with another title that sums up the report: “Federal Reserve and FDIC Should Address Weaknesses in Their Process for Escalating Supervisory Concerns”, while noting that the OCC has procedures already, and largely followed its own procedures.

The Fed is in charge of examining Bank Holding Companies (BHCs), state-chartered banks that are members of the Federal Reserve System, and subsidiaries of foreign banks. The largest banks (national banks) are already supervised by the OCC. The typically-smaller state-chartered banks are supervised by the States, and could be examined by the FDIC as well (which already supervises state-chartered banks not a part of the Federal Reserve System). Too many agencies examining the same bank leads to predictable issues – for example, California’s agency in charge of examining state banks leads its report of the SVB situation by noting that the Fed Reserve Bank of San Francisco assumed a lead role, causing California to step back.

It’s far from clear why the Fed has a comparative advantage, especially in retrospect. The interest rate decisions are hard enough as is. We do not need to make them even harder by having the Fed conflicted that if it raises rates some of its supervised banks will experience bank runs. So let’s let the OCC, the FDIC, and the states manage prudential supervision.

Payments

“FedNow was launched by the Federal Reserve last July to provide real-time payments services in the U.S., enabling transactions to be settled in seconds instead of days…The rival private sector RTP, operated by The Clearing House and owned by major U.S. banks, was started in 2017.”[8] Why is the Fed trying to be a second mover – by six years! – in a market that already has a private-sector solution?

This should be a perfect opportunity for the Fed to let innovation happen in the private sector (where it was already happening much faster), perhaps with the guidance of some appropriate policy goals. This approach worked at the SEC and FINRA for security trading settlement cycles. In 2017, the SEC started to require T+2 settlement (two days) versus the prior T+3. In 2024, the requirement changed to T+1. With enough lead time, the financial industry could figure out faster bank settlements, as it figured out credit card and debit card settlements decades ago, and as it launched RTP six years before FedNow. The Fed could also require some version of fair, reasonable, and non-discriminatory licensing from TCH to non-members including non-bank fintechs.[9]

Consumer Protection

The creation of the CFPB coming out of the financial crisis was an implicit recognition that the Fed did not perform its consumer protection duties. The “Twin Peaks” model of optimal financial regulation suggests having different federal agencies focus on its own regulatory objectives, such as having one agency in charge of prudential regulation and another agency in charge of consumer protection. “Twin Peaks” is heavily emphasized in proposals since the Financial Crisis, including George W. Bush’s Treasury’s blueprint for modernizing financial regulation and arguably including the creation of the CFPB.[10] Management 101: this is how most major corporations organize divisions – there is a finance division, a marketing division, IT department, and so on, each responsible for its own vertical, with this being the standard management practice for decades from Peter Drucker to Andy Grove’s Intel to present-day Amazon.

We have not had major consumer protection blowups since the Financial Crisis, demonstrating that the CFPB is doing its job. And it has continued to do its job even as it lost much of its independence and the Director became answerable to the President. Democratic appointees might push the consumer protection envelope a bit too far, and Republican appointees might swing the pendulum a bit too far the other way. But this is how every executive agency functions, and it’s not clear why we should be making an exception here. Consumer protection concerns took a backseat at the Fed prior to the Financial Crisis, and there is no reason for the Fed to have any responsibility here now that another agency, accountable to the President, is on the job.[11]

Bonus: the Fed’s balance sheet

The Fed went from under $1 trillion in assets in September 2008 to $9 trillion in 2022. The Fed picked winners and losers – a bit more than half of the assets are US Treasuries, and much of the remainder are government MBS (resulting in even lower mortgage interest rates, while renters did not see much of the benefit despite being considerably poorer than homeowners on average). And, bailing financial institutions and investors out for over a decade by increasing asset prices might not be the most sustainable way to ensure financial stability. Regardless of whether one agrees with the choices, these are the decisions that we expect the Congress and the President to make, see for example GM during the Financial Crisis or the airlines during the Pandemic.[12]

An even less controversial fix than simply forbidding the Fed from holding meaningful assets for prolonged periods of time without the President’s or the Treasury’s approval could be constraining the Fed to purchasing only Treasuries, for the purposes of preserving the possibility of something akin to Quantitative easing (QE). QE should be needed (if ever) exactly when the Fed needs to boost the economy more and already lowered rates to 0. In these circumstances, Congress and the President won't stand in the way if asked, while retaining control.

The Fed can preserve its classical lender of last resort (to member banks) mission, even if there are valid concerns over it and a reasonable assumption that the Fed will push it too far. The Fed is now subjected to various requirements, including: only emergency circumstances, only broad-based bank lending (as opposed to lending to individual institutions), sign-off from the Treasury, and informing the Congress within seven days. These requirements should be revisited if they either prove insufficient or too constraining.

Conclusion

This is an opportune time to assign clearer responsibility, trim some regulatory fat, and think through where exactly we need the current Fed-like independence from Congress and the Executive branch. Regulatory rearrangements often happen in the aftermath of a crisis, and thus often end up trying to chase the last crisis’s problem. We should use the current momentum for change to try to get our financial regulation system in order, so that we alleviate future crises, as opposed to simply responding to the last one and then forgetting about it until the next one.

The opinions shared in this article are the author’s own and do not reflect the views of any organization they are affiliated with.

[1] The report was addressed to unnamed “Congressional Requesters.”

[2] The Consumer Financial Protection Bureau (CFPB) was mentioned as a potential target. But why start by hitting “delete” on a more popular agency that spends a maximum of 12% of the Federal Reserve System’s operating budget when you haven’t even looked at the other 88% of that budget?

[3] Bipartisan budget deficits were the primary cause, but arguably the government would not have run such large budget deficits if the Fed Reserve chair had been committed to hiking interest rates.

[4] The Fed reacted too slowly to rising inflation in 2021, and arguably the problem was the exploding government deficit all along. For various views, see: (1) the last-week of administration report from Treasury arguing that this is exactly what the Fed should have done even if it realized the issue earlier, and (2) an argument that actually by the time the Fed reacted it was way too late. Regardless, at the very least the decisive move to raise rates from 0% to 4% in 2022 was considerably stronger than the Fed of the 1970s. The good record of central bank independence also seems to be supported by anecdotal and empirical evidence across the world.

[5] See the Financial Crisis Inquiry Report for much much deeper analysis (and 663 fascinating pages), including a discussion on the role of the affordable housing goals of Fannie Mae and Freddie Mac – a dynamic which the Fed also missed regardless of the role one thinks it might or might not have played. Of course, there were individuals within the Fed who realized each of these dynamics, but that arguably makes the institutional failure even worse.

[6] Dodd-Frank also created the Office of Financial Research (OFR, also within the Treasury), which for many purposes is effectively FSOC’s data, research, and analysis arm.

[7] To anyone who thinks the Fed learned its lesson from 2008, see the Fed’s recent financial stability effort with the Basel Endgame rule. Whatever one thinks about the rule’s merits, the Fed badly mismanaged the process. There were major concerns about the policy on both sides of the aisle, the economic cost-benefit analysis was barely two pages long (a clear indication that the Fed didn’t think it needed to address those concerns) and the result was the entire proposal being scrapped for either a re-work or, more likely, an ignominious death.

[8] See “FedNow pricing aimed at avoiding market disruption,” with the Fed official making it explicit that the Fed isn’t planning the payment system as a competitor to drive TCH’s prices down either.

[9] The Fed operates more payment systems, for example FedACH that provides similar services to EPN (ran by The Clearing House), with both systems a part of ACH that is operated by Nacha (an association owned by private actors). There are other components of the global and US payment systems like SWIFT (ran by an international cooperative) and CHIPS (also ran by The Clearing House). Overall, it’s far from clear where the Fed has a major competitive advantage to industry cooperatives, especially with some government oversight.

[10] See “The Department of Treasury Blueprint for a Modernized Financial Regulatory Structure.” See also, Michael W. Taylor, “The Road From ‘Twin Peaks’ – And The Way Back,” Connecticut Insurance Law Journal (2009), for the original sources of the theory. See “Inside Job: The Assault on the Structure of the Consumer Financial Protection Bureau,” Minnesota Law Review (2019), on the CFPB stemming from this and similar ideas.

[11] In particular, the remainders of consumer protection responsibilities that did not go over to the CFPB should be transferred there – from consumer research similar to what the CFPB already does to the few remaining regulations like the Community Reinvestment Act (CRA) that regardless of how you feel about would fit well with the CFPB’s fair lending enforcement portfolio without the need of the current duplicative supervision, and while being responsive to the President.

[12] As an aside, these assets earned profits while the rates were low. From 2011 to 2021 the Fed transferred to the Treasury about $920 billion in profit (an annual return of under 3%). But after the Fed increased interest rates to fight inflation, it started making losses on these assets, currently at around $200 billion. And then there are unrealized losses – the current value of assets less what the Fed purchased them for – that were at $800 billion at the end of September 2024, and growing. In other words, the Fed had already effectively lost all the money that it made since ramping up its balance sheet in 2008, and then some.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

If an idea matters, you’ll find it here. If you find an idea here, it matters.

Interested in contributing to Open Banker? Send us an email at [email protected].