- Open Banker

- Posts

- When Credit Unions Acquire Community Banks, Local Communities Suffer

When Credit Unions Acquire Community Banks, Local Communities Suffer

Written by Rebeca Romero Rainey

Open Banker

December 09, 2025

In partnership with

Rebeca Romero Rainey is president and CEO of the Independent Community Bankers of America (ICBA), the leading advocacy organization exclusively representing community banks. She is one of the nation’s foremost advocates of the community banking industry, and is a third-generation community banker born and raised in Taos, N.M.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

Across the country, credit unions are using their federal tax exemption to acquire local community banks at an increasing and alarming pace.

Community bankers have long warned that credit union acquisitions of community banks diminish tax revenues, consolidate the industry through tax subsidies, grow the publicly subsidized sector of the financial services industry, and increase the portion of the industry exempt from Community Reinvestment Act (CRA) oversight.

Now, an analysis of publicly available data from federal banking regulators and the Small Business Administration reveals that when tax-exempt credit unions purchase tax-paying community banks, consumers and local communities are harmed. The result is diminished lending, reduced opportunities for small businesses, and fewer resources for the high-poverty areas that Congress specifically subsidizes credit unions to serve.

To expand the tax base and encourage a competitive financial services marketplace, lawmakers should treat credit unions over $1 billion in assets the way they operate — like tax-paying commercial banks.

Tax Subsidies Benefit the Largest Credit Unions

The tax break established by Congress in 1934 was originally conditioned on credit unions operating as not-for-profit institutions that serve people of modest means with a “common bond,” like working for the same employer or attending the same church. However, those standards have slowly eroded under lax oversight, and today many credit unions have virtually zero membership requirements. Consumers hear the jingles marketing “great rates for everyone.”

This evolution is most pronounced at the nation’s largest credit unions. According to an analysis by the Independent Community Bankers of America, where I serve as president and CEO, 451 credit unions held assets exceeding $1 billion at the end of 2024, generating a combined net income of $11.4 billion. While these institutions represent just 10% of all credit unions by footprint, they account for 79% of total credit union net income and 77% of total assets.

By contrast, community banks paid $15.4 billion in income taxes in 2024 and are projected to contribute nearly $90 billion from 2024 to 2028. The cost of exempting large credit unions from income taxes over the same period totals nearly $15 billion.

Growth of Inter-Industry Acquisitions

Despite their taxpayer subsidies, credit unions are permitted to raise money from Wall Street hedge funds and private equity firms and purchase naming rights for professional sports stadiums, including Washington, D.C.’s NFL team. While this raises questions about how credit unions are leveraging their tax exemption, of immediate concern for local communities is how their community banks are being swallowed up by tax-exempt competitors.

While community banks pay their share to Uncle Sam, large credit unions have increasingly used tax savings to acquire local, tax-paying institutions and take their profits off of the tax rolls.

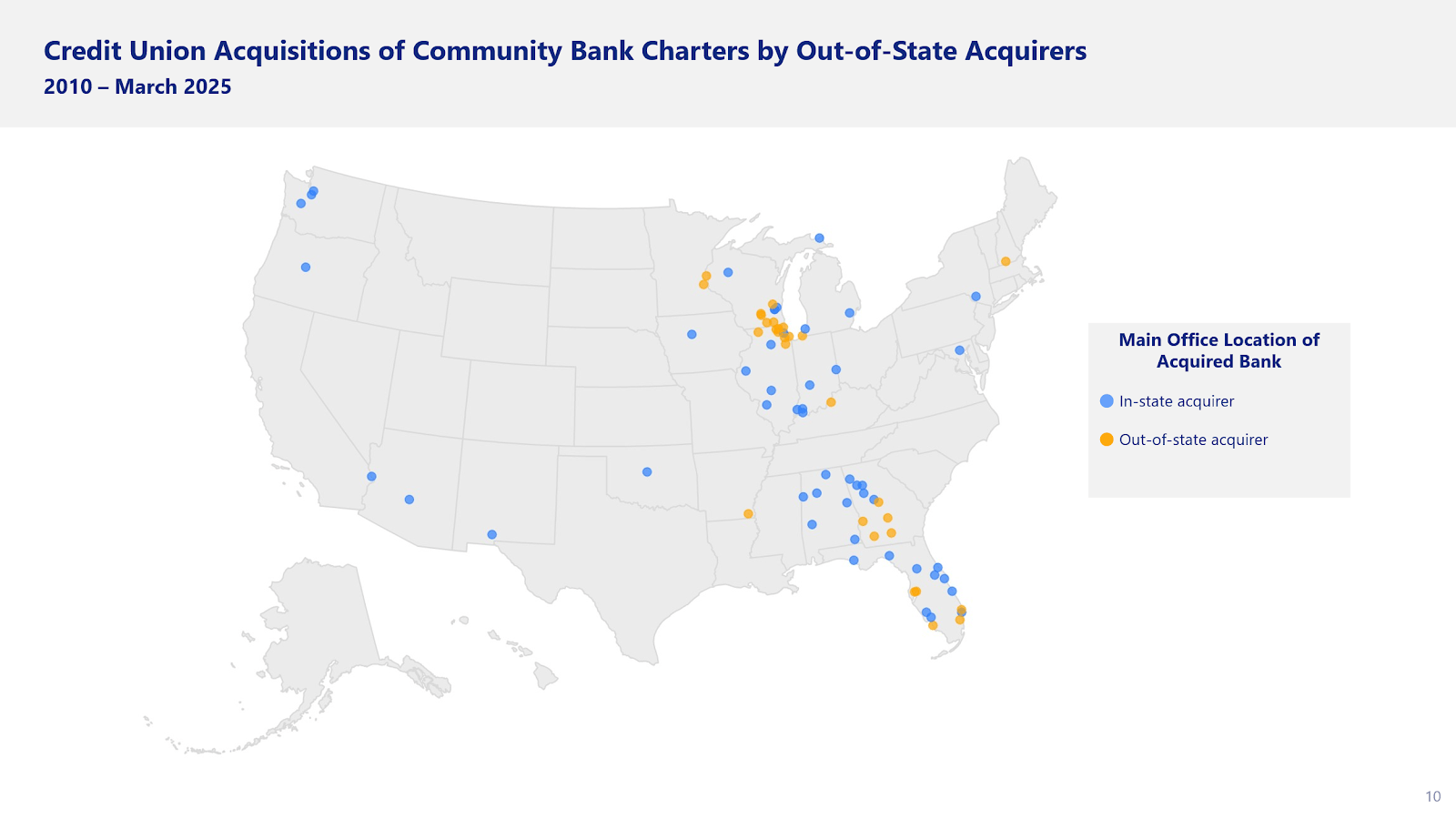

Our analysis of FDIC and Federal Financial Institutions Examination Council data show that credit unions have acquired 77 community bank charters since 2010, with more than 60% of those charter acquisitions occurring in the past five years. In 2024, credit unions announced a record number of community bank acquisitions, eroding local tax bases as the credit union industry’s assets have doubled since 2017.

These transactions often involve the largest credit unions crossing state lines to absorb banks that serve communities well outside their field of membership. More than 80 percent have been driven by credit unions with more than $1 billion in assets.

And despite the credit union industry’s claims, these deals aren’t saving struggling community banks. Nearly two-thirds of acquired banks saw an increase in net operating income in the five years before they were bought, and more than three quarters were actually growing their assets. No wonder their tax-exempt competitors wanted to buy them up.

In other words, the acquired institutions were not “failing banks” in need of saving. They were well-performing competitors, eliminated through acquisition at artificially inflated levels subsidized by the credit union tax exemption.

Harmful Impact on Local Lending

Each acquisition by a credit union not only hampers tax revenues — it also expands the portion of the financial services industry not subject to CRA requirements for lending to low- and moderate-income consumers and small businesses in local markets. Perhaps most concerning for local communities: the data clearly show that when a community bank is absorbed, local lending dries up.

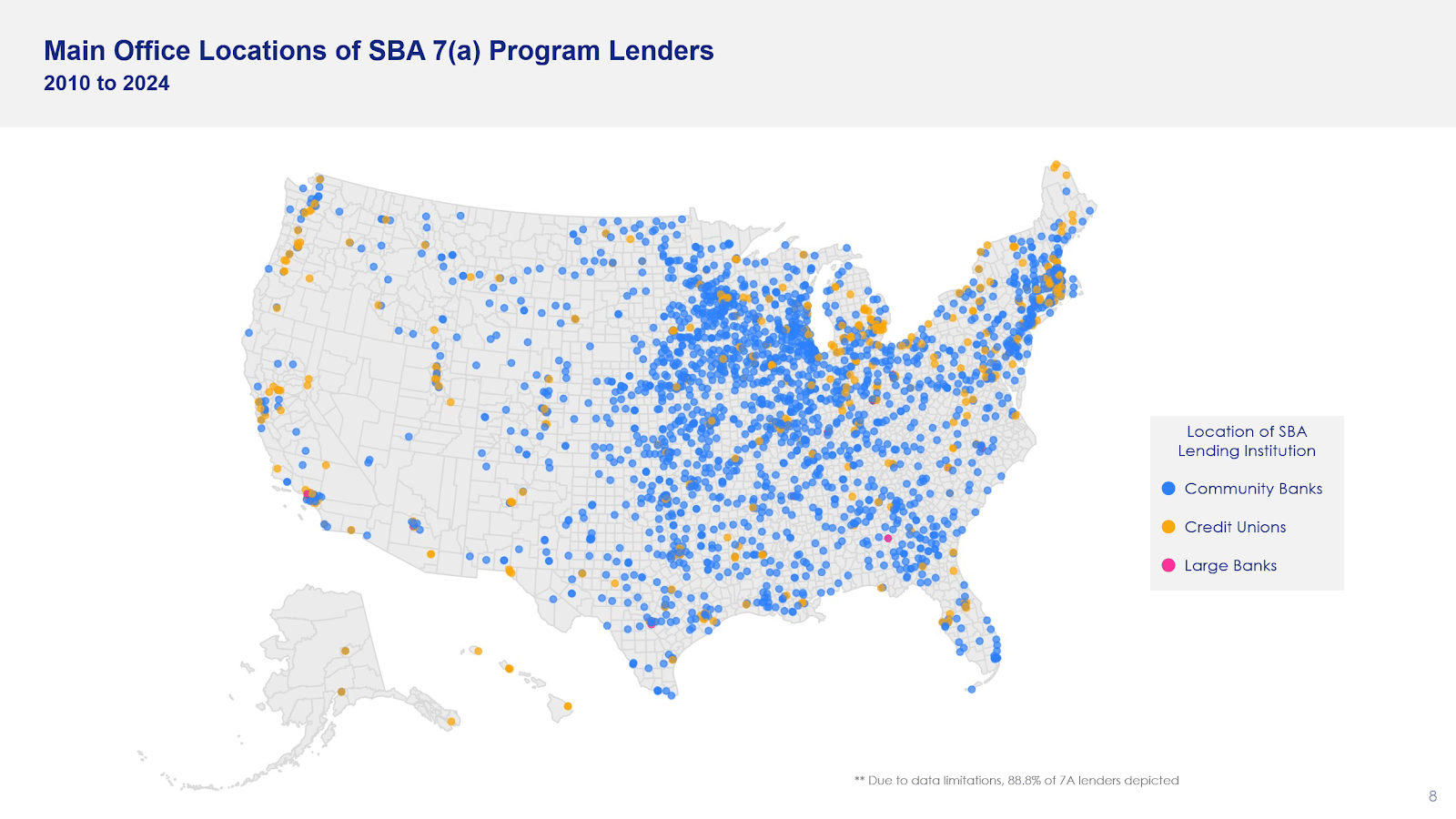

According to our analysis, community banks account for roughly 69.3% of SBA loans provided by banks and credit unions since 2010, compared to 2.8% from credit unions. In markets where community banks participated in SBA programs, those loans declined after a credit union acquisition nearly 80 percent of the time.

Our analysis of Home Mortgage Disclosure Act lending data tells a similar story. In service areas affected by an acquisition:

57% experienced a decrease in total mortgage applications,

the amount loaned per approved mortgage application decreased following 61% of acquisitions,

and the median mortgage loan amount decreased $20,000 per loan.

Most egregiously, mortgage denial rates increased in 61% of acquisitions. In areas where denial rates rose, the median increase was nearly 10 percentage points.

These aren’t just numbers. They represent small businesses unable to expand, families denied a chance at homeownership, and neighborhoods losing an engine of local investment.

Existing Disparities in Serving Low-Income Areas

The impact of acquisitions is particularly concerning given the stark disparities between community banks and credit unions in serving lower-income areas.

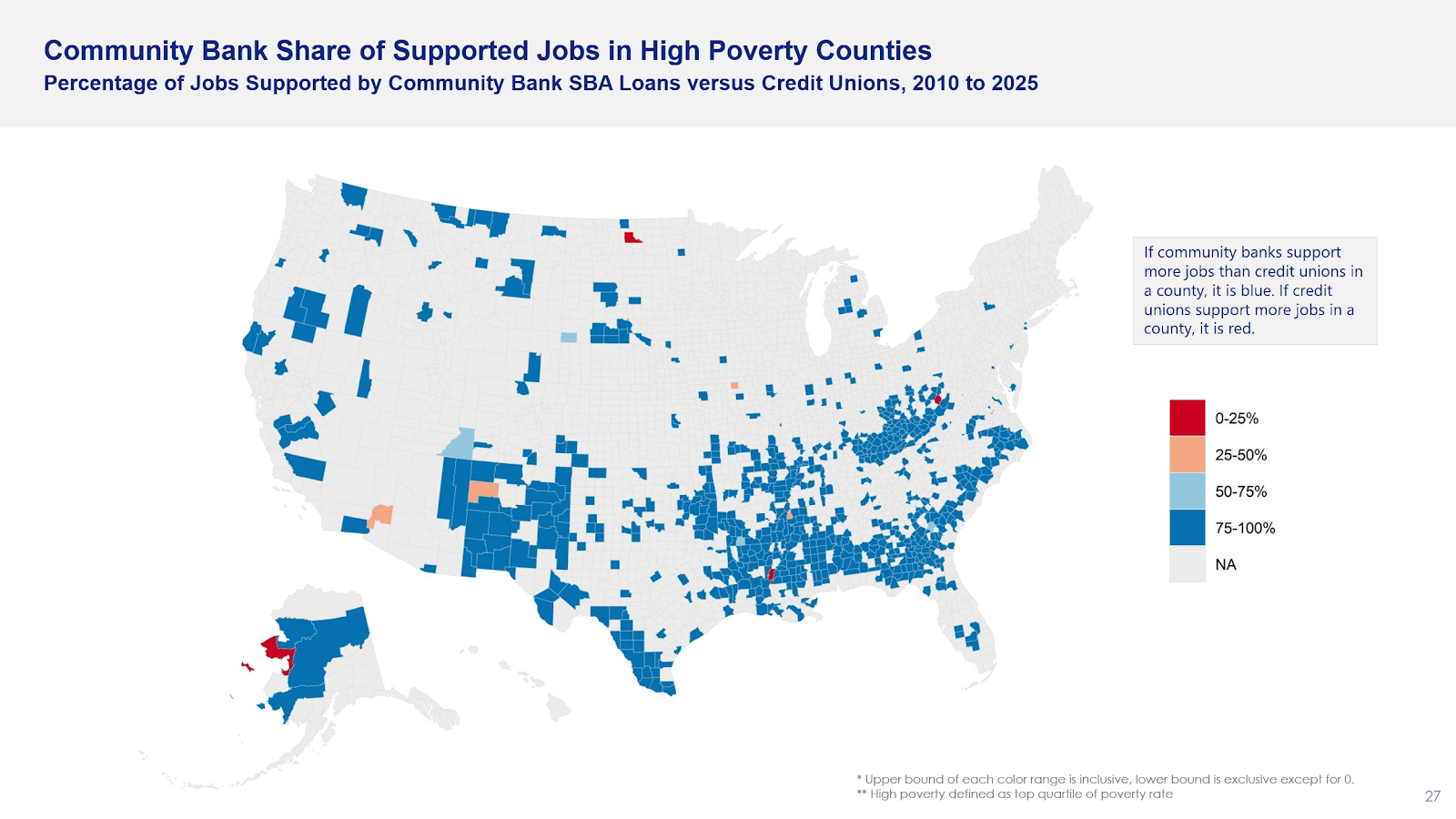

According to our analysis, community banks represented 76.5% of SBA lending in the highest-poverty counties since 2010, compared with just 1.8% from credit unions — showing community banks are outperforming credit unions even in the lower-income communities that credit unions receive a federal tax exemption to serve.

This community bank lending translated to supporting 433,227 jobs in high-poverty areas, compared to just 16,415 jobs supported by credit unions. Overall, community banks issued a total of $305 billion in SBA 7(a) and 504 loans, nearly 25 times more than credit unions. In rural regions, particularly in the Great Plains, the South, and Appalachia, community banks were often the only SBA lenders present.

In other words, credit union acquisitions pose a significant threat to the communities that are most reliant on community banks as an economic lifeline.

Policy Problems Require Policy Solutions

Amid this surge in acquisitions, policymakers are increasingly scrutinizing credit union policies, with the FDIC last year advancing a Statement of Policy on bank mergers that for the first time explicitly stated that additional scrutiny may be needed for deals involving credit unions. And for good reason: this trend is caused not by free and open markets but by public policy. The credit union industry’s tax exemption is tilting the scales in its favor.

With this policy failure demanding a policy response, policymakers should turn the growing skepticism into policy action. Eliminating the federal tax exemption for credit unions over $1 billion in assets will help ensure taxpayer dollars no longer tilt the competitive marketplace, subsidize community banking consolidation, and reduce banking options for consumers and small businesses.

If taxed at the same rate as local community banks, tax payments from the largest credit unions would have totaled $2.6 billion in 2024 — with $580 million going to states and $2 billion to federal coffers. That additional tax revenue could have funded the annual cost of education for 168,338 K-12 students or hired 34,793 police officers.

The Time Has Come for Meaningful Reform

And it’s not just an insider policymaker concern. Consumers increasingly support reforms to credit union policies. Polling conducted by Morning Consult this year found 62% of U.S. adults support a congressional investigation of the credit union industry’s tax and regulatory exemptions.

And given consolidation within the credit union industry itself — with credit unions under $100 million declining by 25% over the past five years while total industry assets have doubled since 2017 — even credit union advocates acknowledge that the industry’s evolution is eroding the rationale for its generous tax benefits.

This would not be the first time Congress has reconsidered financial institution tax exemptions. In 1951, lawmakers revoked the tax exemption for building and loan associations, cooperative banks, and mutual savings banks, finding that these institutions operated much like commercial banks and should therefore be taxed. Precedent exists, and as outlined here, action on credit unions is overdue.

Community banks are proven engines of economic opportunity, especially for small businesses and underserved communities. If policymakers want these local institutions and the jobs, investments, and futures they support to thrive, they must act. Ending tax subsidies for the largest credit unions is not only fair, but also necessary for the health of Main Street America.

The opinions shared in this article are the author’s own and do not reflect the views of any organization they are affiliated with.

Open Banker curates and shares policy perspectives in the evolving landscape of financial services for free.

If an idea matters, you’ll find it here. If you find an idea here, it matters.

Interested in contributing to Open Banker? Send us an email at [email protected].

Start investing right from your phone

Jumping into the stock market might seem intimidating with all its ups and downs, but it’s actually easier than you think. Today’s online brokerages make it simple to buy and trade stocks, ETFs, and options right from your phone or laptop. Many even connect you with experts who can guide you along the way, so you don’t have to figure it all out alone. Get started by opening an account from Money’s list of the Best Online Stock Brokers and start investing with confidence today.